Whether you’re opening your first storefront, expanding to a new location, or investing in commercial property, financing is a critical part of the process. A commercial mortgage is one of the most common tools used by businesses to acquire property. But unlike residential mortgages, commercial loans come with their own rules, requirements, and complexities.

In this guide, we’ll break down everything business owners need to know about commercial mortgages—from the basics to the application process, benefits, risks, and expert tips.

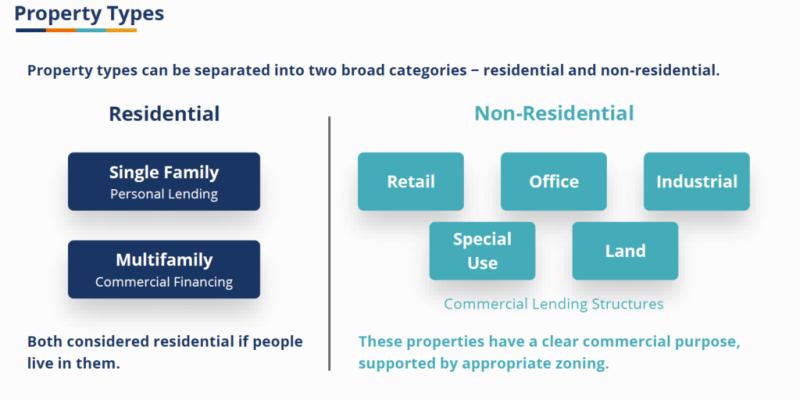

What Is a Commercial Mortgage?

A commercial mortgage is a loan used to purchase, refinance, or redevelop commercial property. Unlike residential mortgages, which are issued to individuals for personal homes, commercial mortgages are designed for business purposes.

These loans are typically used for:

- Office buildings

- Warehouses

- Retail spaces

- Hotels

- Multifamily units (usually over 5 units)

- Industrial sites

In essence, a commercial mortgage allows a business to borrow money to buy or improve real estate that will be used for generating income.

How Does a Commercial Mortgage Work?

Commercial mortgages function similarly to residential ones but with stricter terms and more complex underwriting.

Key components include:

- Loan Term: Typically shorter—5, 10, or 20 years, with amortization periods sometimes longer.

- Interest Rates: May be fixed or variable, but often higher than residential loans.

- Down Payment: Usually 20–40% of the property’s value.

- Repayment Structure: May include balloon payments (large final payment).

- Collateral: The property serves as the main collateral. In many cases, personal guarantees are also required.

Most commercial mortgages are non-recourse, meaning the lender can only seize the property if you default—but many lenders will still require personal liability clauses for small businesses.

Types of Commercial Mortgages

There are various types of commercial property loans available, depending on your business needs and credit profile.

Traditional Commercial Mortgage

Issued by banks or credit unions, these offer competitive rates but require strong credit, financials, and business stability.

SBA Loans

Backed by the Small Business Administration, SBA 504 and 7(a) loans are ideal for small businesses, offering low down payments and favorable terms.

Commercial Bridge Loans

Short-term loans for businesses that need fast access to capital—often used for time-sensitive acquisitions or renovations.

Hard Money Loans

Funded by private investors. Higher interest rates and fees but quicker approvals and less stringent documentation.

CMBS Loans (Commercial Mortgage-Backed Securities)

Packaged into mortgage-backed securities. These loans are attractive for larger deals but come with rigid terms and less flexibility.

Eligibility Requirements

Securing a commercial mortgage requires proving that your business is financially sound and that the investment is low-risk for lenders.

Common requirements include:

- Strong Credit History (Business and sometimes personal)

- Business Plan with projections

- 2–3 Years of Financial Statements

- Proof of Income or rental income (for investment property)

- Down Payment (20–40%)

- Collateral Appraisal and possibly environmental reports

Lenders may also assess your Debt Service Coverage Ratio (DSCR)—a measure of how easily your business can cover loan payments. A DSCR of 1.25 or higher is usually preferred.

Benefits of a Commercial Mortgage

A commercial mortgage offers several long-term advantages for business owners looking to establish or expand their footprint.

Key Benefits:

- Equity Growth: As you repay the loan, you build equity in the property.

- Stability: You avoid fluctuating lease rates and gain control over the premises.

- Tax Benefits: Interest payments and depreciation may be tax-deductible.

- Leasing Opportunities: You can lease part of the space to other tenants.

- Appreciation: Commercial real estate tends to appreciate over time.

If your business is stable and profitable, owning your commercial space can be more cost-effective than leasing.

Risks and Challenges

Like any financial product, commercial mortgages come with risks that business owners must evaluate carefully.

Major Risks:

- Large Down Payments: Tying up cash that could be used for operations.

- Balloon Payments: Unexpected large final payments if not refinanced.

- Interest Rate Fluctuations: If your loan has a variable rate.

- Vacancy Risk: If you’re relying on tenant income to repay the mortgage.

- Maintenance and Repairs: As the owner, you’re responsible for all upkeep.

Additionally, if your business struggles and you default, the lender may foreclose on the property—and personal guarantees could put your personal assets at risk.

Steps to Secure a Commercial Mortgage

Navigating the process of getting a commercial mortgage can feel daunting, but breaking it down into steps makes it manageable.

Step 1: Assess Your Financial Readiness

Before applying, ensure your credit, financial records, and business plan are solid.

Step 2: Choose the Right Lender

Compare banks, credit unions, and private lenders. If you’re a small business, look into SBA-backed options.

Step 3: Get Pre-Qualified

Lenders will give you an estimate of how much you can borrow based on preliminary information.

Step 4: Property Appraisal and Due Diligence

An independent appraisal determines the value. Environmental assessments and inspections may also be required.

Step 5: Submit Documentation

This includes:

- Tax returns

- Profit & loss statements

- Balance sheets

- Rent rolls (for rental properties)

- Business licenses

Step 6: Underwriting and Approval

The lender evaluates your risk and may ask for additional information.

Step 7: Close the Loan

Sign the documents, pay closing costs, and finalize the transaction. You now own the property!

Conclusion

A commercial mortgage can be a game-changing tool for business owners looking to build long-term stability and value. It enables you to invest in your future, reduce reliance on landlords, and potentially generate passive income through leasing.

However, it’s not a decision to take lightly. You must consider your business’s financial health, market conditions, and long-term goals. With the right preparation, guidance, and strategic planning, a commercial mortgage can set the foundation for sustained growth and prosperity.

If you’re ready to move from renting to owning—or want to leverage property as a strategic asset—exploring your commercial mortgage options is a smart next step.

FAQs

1. What is the difference between a commercial and residential mortgage?

A commercial mortgage is used to buy or refinance property for business use, while a residential mortgage is used for personal homes. Commercial loans usually have shorter terms, higher interest rates, and larger down payments.

2. How much deposit do I need for a commercial mortgage?

Typically, you’ll need 20% to 40% of the property’s purchase price. SBA-backed loans may allow for lower down payments.

3. Can a startup get a commercial mortgage?

Yes, but it’s more challenging. Startups may need to provide a strong business plan, collateral, and personal guarantees. Alternative lenders or SBA 7(a) loans may be more flexible.

4. Are commercial mortgage interest rates fixed or variable?

They can be either. Fixed-rate loans offer predictable payments, while variable rates may start lower but can rise over time. Your lender will help you choose based on risk tolerance and goals.

5. Can I lease part of the property I buy with a commercial mortgage?

Yes. Many business owners lease out unused portions of their property to generate additional income, which can also help with mortgage repayments.

Also read: Is GetYourGuide Legit? 10 Things You Didn’t Know About Its Legitimacy